This year saw a supply-demand balance in the copper market, which is set to transition into a major supply surplus in 2024, according to the International Copper Study Group (ICSG).

After hitting a record high of US$10,730 per metric ton in early March on the London Metal Exchange (LME), prices have dropped 21% to US$8,450 per metric ton as of late June, a level US$300 below where they were projected to be.

BloombergNEF, a strategic research provider, highlighted copper’s price volatility throughout 2023, pushed by China’s slow economic recovery and the bleak economic outlook in the US. However, prices are expected to climb to a modest recovery in 2024 as burgeoning demand from the energy transition offsets global economic weakness.

The ICSG met in Lisbon, Portugal in early October for its second gathering of the year; joining government representatives and industry advisors from the world’s leading copper producing and consuming countries to discuss the outlook for copper as the new year approaches.

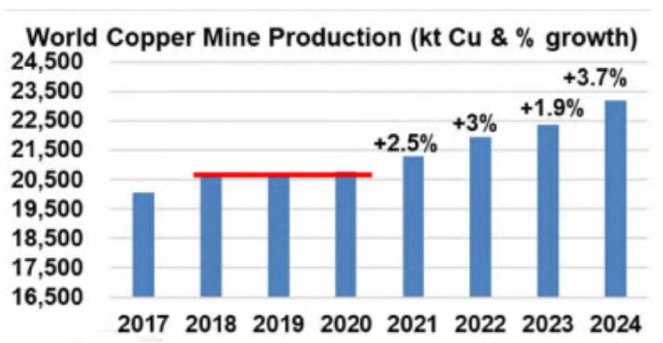

The group predicted that world mine production in 2024 will increase by 3.7% due to additional output from new and developed mines in the Democratic Republic of the Congo (DRC), Peru, and Chile, for example. Production rates are also expected to improve in countries affected by operational constraints in 2023; namely Chile, China, Indonesia, Panama, and the US.

Notable projects starting or expanding over the two-year period between 2022-2024 include Kamoa Kakula and Tenke in the DRC; Quellaveco and Torromocho in Peru; Quebrada Blanca QB2 in Chile; as well as Malmyzhskoye and Udokan in Russia. A number of medium and small projects along with expansions will also add to copper output. Most of the projects starting in this period will be concentrate producing mines.

The increase in production will exceed consumption by 467,000 metric tonnes in 2024, a significantly higher analysis than the originally anticipated 297,000 metric tonnes surplus at the time of the group’s last meeting in April.

According to the group, the two main trends in the market are: the weakening of Western copper demand and the strengthening of Chinese copper production.

Chinese strength

China is in the midst of a rapid expansion of its copper industry, one which is reshaping global channels of the essential red metal for the world’s green energy transformation.

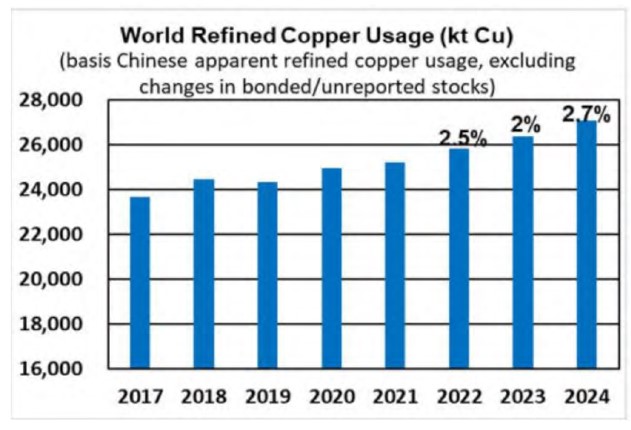

Earlier this year, the ICSG expected copper demand outside of China to rise by 1.6% in 2023 after only 0.4% growth the year before. Six months on, copper consumption has not quite reached those targets, with expected 1% contractions from last year’s figure.

However, faltering Western demand is being counteracted by Chinese demand, which is forecast to grow by 4.3% this year. Overall, global growth for 2024 remains optimistic with predictions in refined usage projected at around 2.7%.

This assessment resonates with the copper market consensus that Chinese demand unexpectedly tilted to the upside this year. Copper’s key role in the green energy sectors such as solar panels, wind power, and electric vehicles (EVs) seems to have preserved the metal from a manufacturing dip.

With a further up-tick in factory activity likely, China will continue to be the key driver of global copper demand in 2024 as high interest rates impede manufacturing activity in both Europe and the US.

Swell in refined copper production

The anticipated increase in copper consumption throughout 2024 is still expected to be overshadowed by a 4.6% jump in global refined copper production, with a production surge already in progress.

As with demand, rising metal production is mostly credited to China, which continues to advance its smelting and refining capacity. The country’s output rose by approximately 11.5% year-on-year in the first eight months of 2023, according to local data provider Shanghai Metals Market (SMM), and smelters are continuing to ramp up production.

Next year will follow a similar trend of intensifying global copper production, with momentum from new smelters and capacity expansions in Indonesia, India, and the US. The amount of copper produced from recyclable materials will also contribute to the increase due to investment in new secondary smelters and refineries.

Overall, an extensive supply excess has been anticipated for 2024 by most analyst groups, taking the market by surprise after the operational constraints of 2023.

However, analysts recognize that that these forecasts are snapshots in time and note “that actual market balance outcomes have on recent occasions deviated from ICSG market balance forecasts due to unforeseen developments.”

The ICSG’s October announcement adds to a growing discourse that the copper market is heading into a period of fast-rising production and uncertain demand in the world outside of China. The energy transition provides a safety net for the metal, but the balancing act of supply and demand weighs on the market.

{kind=link}