The global nickel market has a volatile history which has experienced periods of prolonged growth followed by sustained periods of lows. The Assay breaks down market and demand trends for nickel over the last few years, giving an in-depth breakdown of the metal characteristics and uses.

Understanding nickel

At number 28 on the periodic table, nickel is a silvery-white, ductile, and malleable ferromagnetic metal with the symbol Ni. Nickel is an excellent conductor of heat and electricity, is bivalent, and is harder in substance than iron.

A sought-after property of nickel is its ability to resist corrosion at high temperatures. It is frequently associated with coinage but is also used in various other applications, particularly stainless-steel alloys and other domestic/industrial industries.

According to The Nickel Institute, nickel will immediately alloy with many other metals, including iron, chromium, molybdenum, and copper. Alloying nickel with other materials creates metals resistant to corrosion and maintains exceptional high-temperature strength along with other unique properties, such as shape memory and low expansion.

There are several different variations of nickel products, the most common being:

- Wrought nickel

- Nickel-pig iron

- Nickel-iron alloys

- Nickel-copper alloys

- Nickel-molybdenum alloys

- Nickel-chromium alloys

- Nickel-chromium-iron alloys

- Nickel-chromium-cobalt alloys

- Nickel-titanium alloys

What is nickel used for?

The Royal Society of Chemistry (RSC) states that nickel is commonly used to plate other metals to protect them from corrosion, however, it’s main purpose worldwide is to make alloys like stainless steel.

RSC explains that nichrome is a common alloy created by combining nickel, chromium and silicone, manganese, and iron. Due to the application of nickel, nichrome resists corrosion, even under extreme temperatures, which has led to it being used in many heat-intensive applications, such as ovens.

A copper-nickel alloy is frequently used in salt removal plants, transforming seawater into freshwater. Other alloys of nickel can be used in boat propeller shafts and turbine blades.

Lithium-ion batteries, used by many major electric vehicle (EV) makers, use a cathode predominantly composed of nickel, which is skyrocketing demand for the commodity.

However, not all nickel is suitable for producing lithium-ion cathodes and there are also other forms of lithium-ion batteries that do not use nickel in their cathode make up.

Historical nickel prices

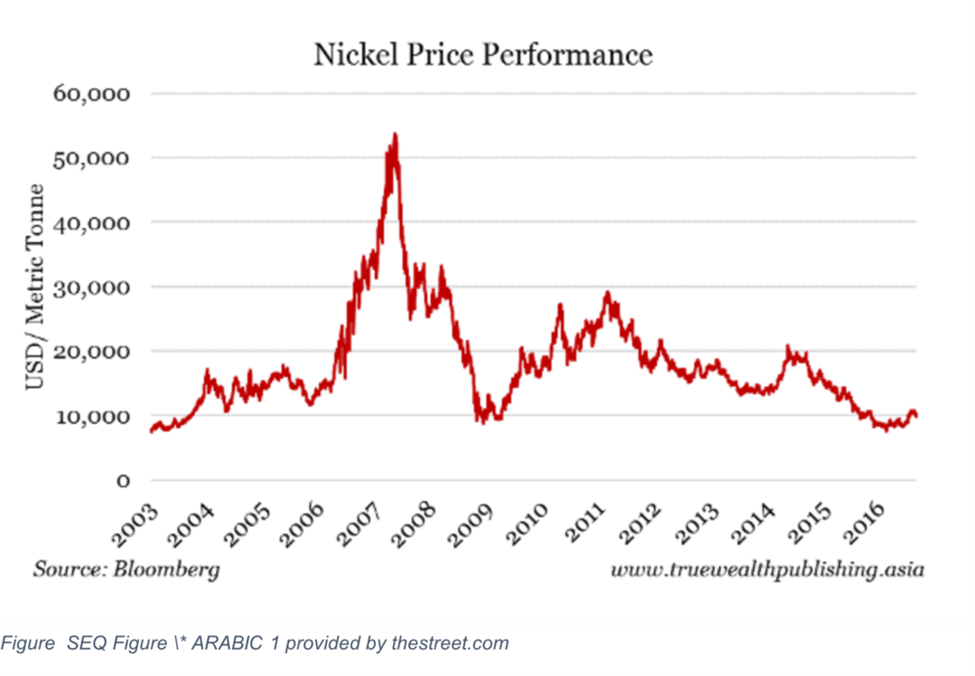

Nickel prices have experienced turbulence over the last few years, undergoing significant highs and lows since the pandemic. Below is a graph provided by Bloomberg, which shows nickel price performance from 2003 to 2016.

Nickel hit an all-time high in 2007, with commodity prices per metric tonne reaching US$53,750. Comparatively, in 2016, prices decreased by a substantial 82%. Reuters reported the reason for this significant decline, stating that between 2015-2016 prices for nickel crashed by 40% alone due to rising stockpiles and weak Chinese demand.

The nickel market picked up in 2016 and 2017 after a considerable period throughout 2015.

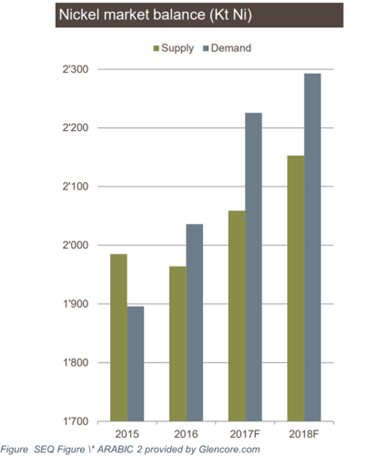

Glencore (LSE: GLEN) provided a table showing the market balance for nickel supply and demand from 2015 to 2018.

The market balanced out from 2016, where demand significantly surpassed supply capacities in 2017. This stabilization was primarily due to environmental crackdowns in China’s stainless-steel sector and NPI production, accounting for an estimated 50% of global consumption.

The combination of large closures of supply (over 200Kt) and a steady resurgence in global demand led to an exceptional recovery in the nickel market from 2016 to 2019, with prices at one stage doubling from their lows.

Since 2018 to 2020 the nickel market has remained tempestuous, according to economic data provided by FRED, which is expressed in the table below, with the market soaring from April 2020 onwards.

Nickel in the present day has come a long way and is now unfortunately in a slump due to decreasing EV production.

According to the National Bureau of Statistics (NBS), China’s production of new energy vehicles increased by only about 30% in 2023. This is down compared to the 2.5-fold increase in 2021 and the near doubled production in 2022.

The decline in nickel demand is further compounded by the slumping property market in China, as nickel is also used in stainless steel for industrial equipment and building materials. According to the NBS, investment in real estate development in China sank by 9.6% last year.

This decrease in property market activity has had a direct impact on the demand for nickel, adding to fresh challenges faced by the industry.

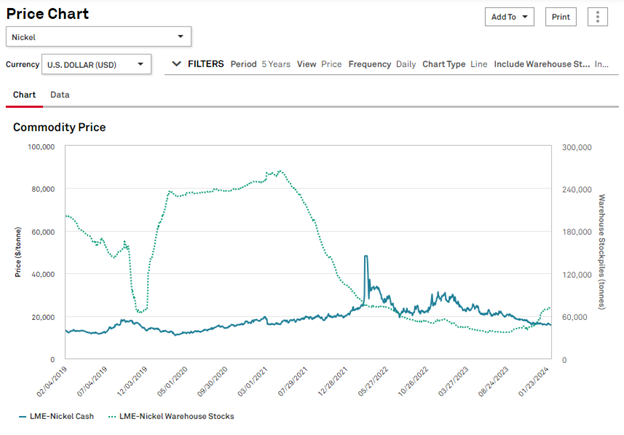

Nickel spot price

The most recent spot price per tonne of nickel in February 2024, reported by S&P Capital, is US$115,380/t. The future contracts for nickel will depend on possible oversupply of nickel (predominantly out of Indonesia), decreasing stainless steel demand, and slowing EV demand.

Nickel supply

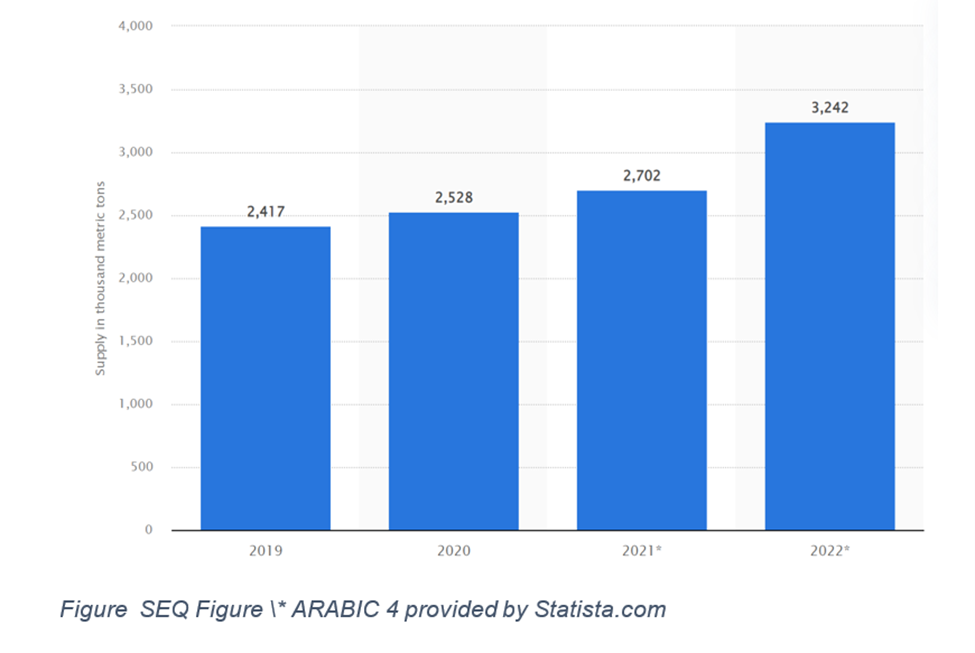

Nickel supply has gradually increased over the last few years. According to Statista.com, the worldwide supply of nickel amounted to almost 2.53M metric tonnes in 2020. It was originally projected that the nickel supply would increase to roughly 3.24M metric tonnes globally in 2022. Actual rates are nearly spot on and have grown further still.

The January 2024 US Geological Survey (USGS) reported that the worldwide mine production of nickel in 2023 was assessed at 3.6Mt. Indonesia was the most significant producer at 1.8Mt, or 50% of global mined production followed by the Philippines with 400Kt or 11%.

In January 2019, the USGS report noted that Vale (NYSE: VALE) mining in Indonesia’s Central Sulawesi Province initiated a project to generate nickel use in batteries. According to the USGS, various mothballed facilities and postponed development projects commenced activity in the hope of riding the wave of growing demand for nickel in EV batteries, therefore boosting worldwide nickel supplies.

Nickel mines in the world

According to S&P Capital’s mining database, these are the largest nickel projects by reserves and resources:

- The SLN mine – ERAMET S.A., Societe Territoriale, and Nippon Steel Nisshin Co. (ENXTPA: ERA)

The mine is in the French territory of New Caledonia in Oceania and produced an estimated 40.9Kt of nickel in 2022 and contains 19.98Mt of contained nickel in reserves and resources.

- The Polar Division mine- Russian nickel company, Norilsk Nickel (MISX: GMKN)

The mine is both open pit and underground in Krasnoyarskiy Kray, Russia and produced an estimated 63.85Kt of nickel in 2022. The mine has 16.7Mt worth of contained nickel in reserves and resources.

- The Weda Bay mine – Tshingshan Holding Group, ERAMET S.A., and PT Aneka Tambang Tbk

The open pit mine is in Maluku Utara, Indonesia and produced 36.6Kt in 2022 with a contained nickel reserve and resource of 15.18Mt.

The shortfall or overexploitation of these large and prominent nickel mines can greatly affect nickel supply worldwide as the collective whole makes a shift towards net-zero and its vital role in the green energy transition.

Nickel demand

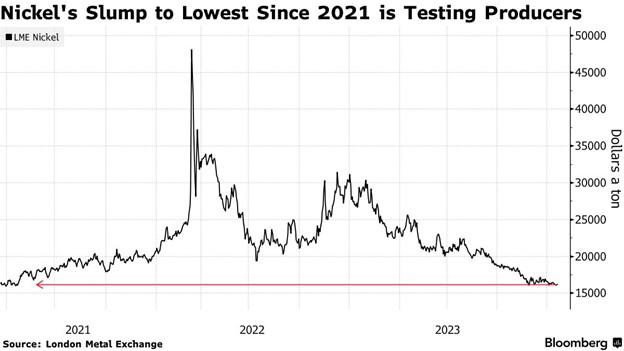

The global nickel market is facing challenges due to an excess supply of nickel from Indonesia and softer demand growth from the EV sector, Bloomberg reported. This oversupply has led to low nickel prices, hovering under US$16,000/t, the lowest levels since 2021.

BloombergNEF warns that nickel producers have already started to slow down production, evident with with BHP, the world’s largest miner, suspending parts of its Kambalda concentrator due to halted ore supply and is reviewing its Nickel West business.

Another mining giant located nearby in Western Australia is First Quantum, who also announced the suspension of its Ravensthorpe nickel facility along with workforce reductions.

Investment bank, Citigroup Inc., sees the nickel price hitting US$15,500/t sometime in Q1 2024 after having already dropped average price estimates to US16,000/t, down from US18,000/t.

Future of nickel

Despite stagnant metal prices in 2024, there may be potential benefits, according to S&P Global Mobility. EV margins may actually prove to be positive, but at the threat mining project viability.

The decline in battery metals prices has had a significant impact for metals like lithium, cobalt, and nickel where some have come down a significant amount in the past year alone. The stagnant metal prices may help reduce EV battery costs, thereby improving affordability if the savings are passed on to consumers.

A common complaint for potential EV consumers has affordability at the top, followed by charging infrastructure, and range. However, this affordability would come at the potential expense of new mining projects, which may face suspension or delay as is already being seen among different nickel companies.

Nickel market outlook & price forecast

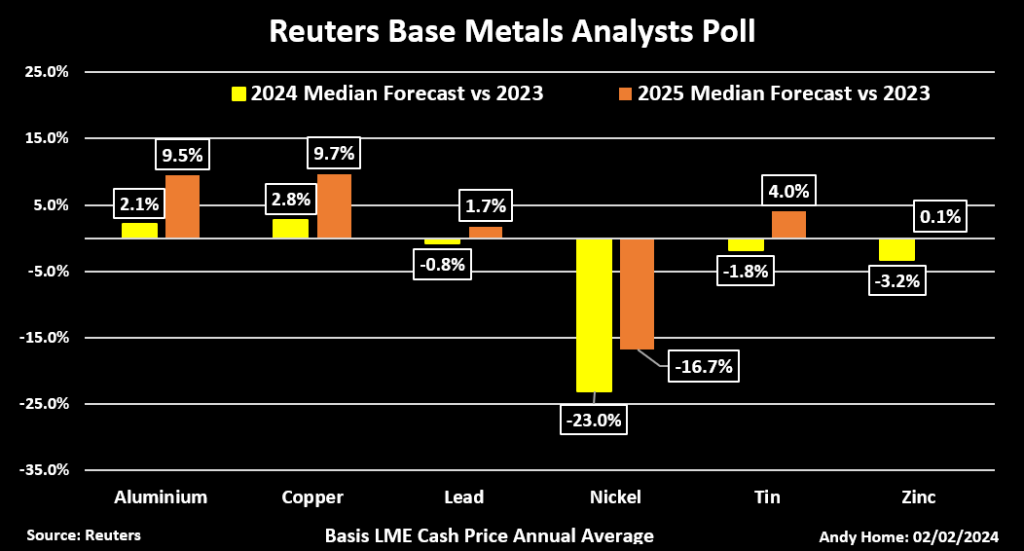

Based on a Reuters analyst poll, looking forward, the market is expected to be flooded with new nickel supply, leading to an estimated surplus of 240.5Kt in 2024 and an additional surplus of 204Kt in 2025. There are already cuts happening to mine supply worldwide with the potential for further cuts.

As the nickel and battery mining industry faces a scramble for funding, attention is increasingly turning to investors who are still willing to invest in battery-related ventures.

Bloomberg noted that Saudi Arabia has emerged as a significant player in this regard. The country’s efforts to diversify away from fossil fuels have led to strategic moves, including the acquisition of a 10% stake in Vale SA’s nickel and copper business. This development solidifies Saudi Arabia’s position as a pivotal player in the industry.

Overall, the outlook for nickel remains bearish in the short term with the market predicted to remain in surplus. This oversupply presents a challenge for nickel, and the market may require a significant fall in prices to rebalance. Although prices are not expected to fall much further, a sustained rally in prices appears unlikely due to the growing weight of the surplus.

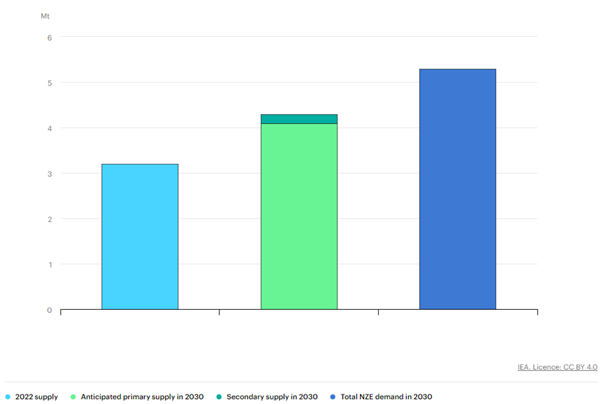

Anticipated supply and projected demand for nickel in the Net Zero Scenario, 2030

While most battery markets are currently in surplus, shortages have already been widely forecast as 2030 edges closer and as the demand for greener technologies continues to rise with countries pushing towards ambitious climate goals.

A rebound is predicted towards the later end of the decade, with the International Energy Agency anticipating demand will comfortably surpass supply.

For more information on nickel, look at our nickel news centre.

{kind=link}

Comments 2