Uranium is commonly touted in the media as a key plank in the transition to a low-carbon economy and the growth in energy demand for data centres driving Artificial Intelligence (AI) models. The latest ABS Capital Expenditure report (May 2024) highlighted that data centres have seen a 60% growth in capital expenditure year on year. Unknown future demand is causing many macro forecasters and analysts to predict bullish medium- to long-term outlooks for the commodity.

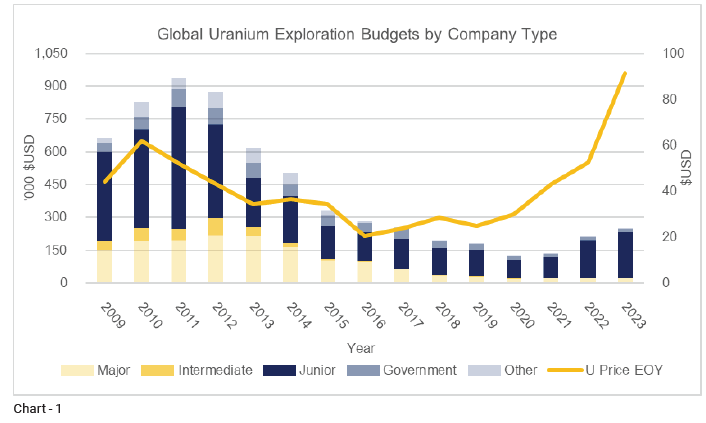

However, there is an issue. The uranium sector has seen over a decade of under-investment post the 2011 Fukushima incident as demonstrated in Chart 1 below. Global exploration expenditure fell rapidly post 2012, with a minor recovery from 2022, lagging the recovery in the uranium price from 20201.

Most of this historic exploration expenditure has come from junior companies, not the majors. At Acorn Capital, we know that junior uranium companies have been in a bear market for most of the last two years, making funding particularly hard and thereby slowing down investment in pre-production activities, such as drilling, permitting, and studies.

Barriers to entry

In addition, it now takes over 16 years, on average, to bring a mine into production from discovery2. The key reasons for the long timelines are delays associated with exploration, development studies, permitting, and financing. All these activities are essential to progress the projects, but during a bear market it can be very difficult to fund the activities.

Moreover, for uranium companies, these activities can often take even longer than for other commodities. For example, many jurisdictions have bans on the mining of uranium deposits that can inhibit resource definitions and mining studies.

The investment opportunity

As specialist resources investors at Acorn Capital, we are acutely aware of how hard it is to get mines into production, let alone making a discovery in the first place. So, how can Australian investors get exposure to this undersupplied market and the investment opportunity Uranium presents?

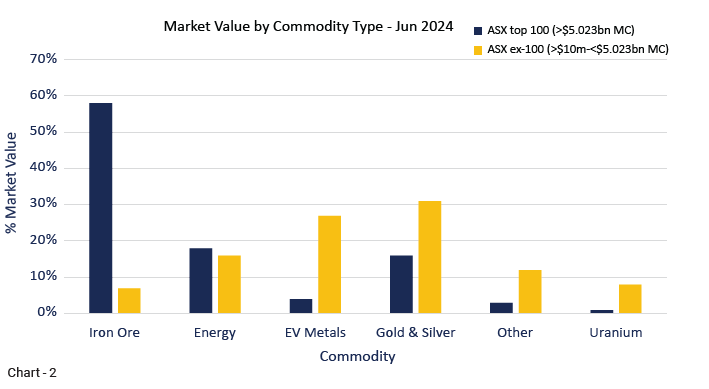

On the ASX there are a total of 31 uranium-focused companies, with only one company sitting in the ASX 100 universe. The rest are outside the top 100 on the ASX. Chart 2 shows the commodity composition of the ASX 100 & ex-100 (>US$10MMC-<US$5.3B) by market capitalization.

This chart shows how investors can get exposure to the smaller and less-capitalized end of the market to get direct exposure to uranium companies.

Three companies have recently moved into production: Boss Energy, Paladin Energy, and Peninsula Energy. All three mines were in production prior to the Fukushima incident but closed when prices fell below US$25/lb post 2011. The capital required to restart these operations was significantly lower than greenfield sites as the plant and mining infrastructure were already in place along with the extremely difficult to obtain mining licences.

These three developers raised their capital from equity markets with other funding sources, such as debt or customer pre-payments, playing minor roles in moving these projects into production. Investors in these companies need to be aware of cost inflation or commissioning risks as they move to nameplate production, but stock prices have already largely re-rated.

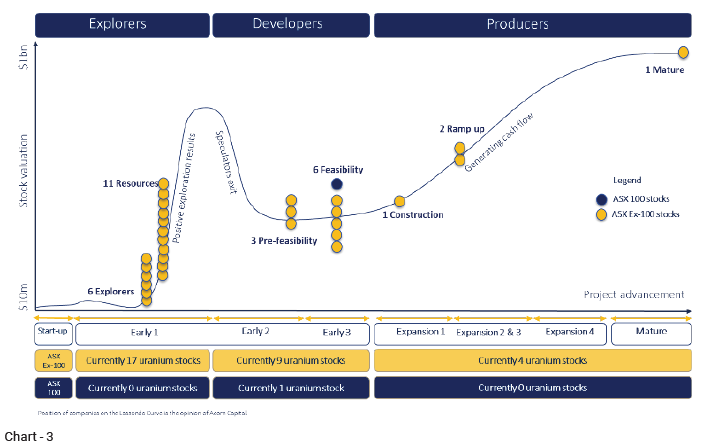

Chart 3 below shows the ASX uranium companies by our proprietary stage of development classification.

Nine companies are progressing through scoping, pre-feasibility, or definitive feasibility stages. All of these developers will need to raise capital to move their projects into construction and on to cash flow generation. Most of that funding will be sourced from private equity markets with little or no participation from debt or offtake providers. Additionally, many of these developers are greenfield sites with the quantum of capital required for production being materially higher than for the three companies already expanding.

These developers have years before they achieve their final permitting approvals and complete the engineering studies to be ready for final investment decision and financing. Investors in these companies must be patient and recognize that substantial funding rounds are needed to progress these projects and achieve shareholder returns.

The technical risks to be aware of include metallurgical, mining, permitting, jurisdiction alongside the financing risks. Furthermore, there is no guarantee that all these projects will get funding, and even if they do, not all will successfully get into production. There are many risks around cost over runs or technical challenges associated with mining and metallurgy.

Of the 31 companies listed on the ASX, over half are explorers and undeveloped. Many had invested in their uranium assets prior to 2011 and been mostly in hiatus due to the low commodity price or have pivoted to another commodity to explore in their nuclear winter. They are only now starting to emerge from that winter and dust off their uranium assets. These explorers have been unable to progress activities, such as studies or permitting applications. Despite this, explorers present a high-risk investment opportunity for investors as the discovery phase is often where large share price movements can be seen on the back of good drill results.

At Acorn Capital, we believe that the barriers to production for the uranium sector has created a structurally short market. Investors have several companies to choose from, but almost all are outside the ASX top 100 and are at various stages of development. Each of those stages have numerous risks from discovery to metallurgy to permitting and jurisdiction as well as the all-important financing. Acorn Capital has been investing in resources for over 20 years focused solely on identifying and assessing the technical and financial risks of these companies.

{kind=link}