You remain positive on gold and silver – what makes you retain this position year on year?

My commitment to gold investing stems from the fact that it is one of the oldest assets in existence. From its use as a currency in ancient times to its investment use and utility today, gold is a “hard” asset and has always served as a store of value. The 21st century has been marked as an age of excessive leverage and money printing, with the recent COVID-19 pandemic accelerating government spending and leading to record levels of Central Bank balance sheets. This is bringing into question the full faith and credit of fiat currencies and government bonds.

Talk about the role of gold (and other precious metals) in a diversified portfolio. Do you think it still holds value as a safe-haven asset?

Many major asset classes are highly correlated, which means that they tend to move in the same direction at the same time. This is because many assets, like stocks, real estate or commodities, all tend to rise and fall with economic performance and investor sentiment. The price of gold is driven by different factors than many major assets. Therefore, gold’s performance moves independently and helps serve as a return diversifier within a broader multi-asset portfolio.

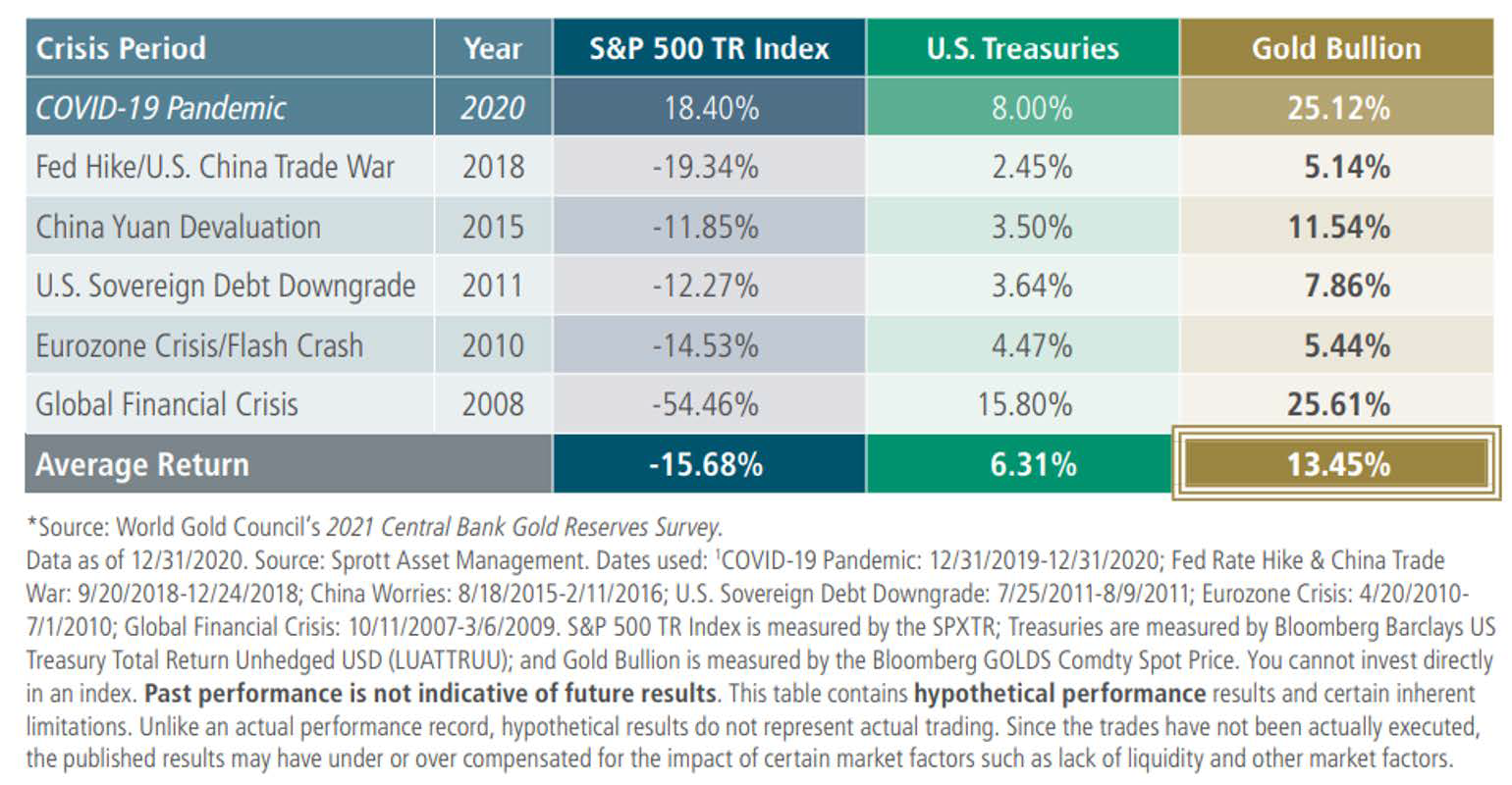

Investors seek out gold for its safe haven quality during periods of economic and political instability. During the height of the COVID-19 pandemic crisis, gold outperformed both stocks and bonds. According to the World Gold Council,* gold’s performance during periods of crisis has risen to become the “top reason for central banks to hold gold”. (See chart below.)

Do you see any challenges to the precious metals markets coming up in the near-term?

The precious metals markets have been challenged by high inflation (an aftermath of excessive debt, money printing and global supply chain disruptions) leading to many central banks, including the Fed and the Bank of Canada, adopting hawkish stances. The Fed is scrambling to combat inflation by raising interest rates and quantitative tightening. The U.S. dollar has been strongly contributing to gold’s weakness. High inflation has also impacted miners’ earnings, particularly on the development side, where both capex and opex have been climbing. This, however, is starting to reverse with energy prices pulling back and miners indicating a stronger second half of the year.

In light of this, what position will the Fed take going forward and do you see any relief coming in?

The quick pace of interest rate increases is causing a sharp downturn in economic and financial activity, from the housing sector to consumer spending, negative GDP prints and a declining stock market. The Fed is raising rates above the neutral rate and I think the carnage is just beginning. At some point, I expect the Fed will have to backpedal. The question is what will it take? Certainly, a Fed pivot would be very favourable for the precious metals as has been the case in 2018/2019, for example.

At the same time, physical demand for gold has been strong, particularly in China and India where the metal has been commanding a premium and Chinese gold imports have been increasing. The physical demand is providing a floor to the gold price, so when sentiment changes, I think we can expect new highs in the gold price.

What’s the outlook for the junior mining space under the current conditions? Where do you see the most stand-outs coming from and what makes a junior stand out to you?

I am a big fan of juniors that have low general and administrative expenses and put the most resources into the ground. When gold and silver prices rose after the pandemic, many companies were able to raise money for exploration, which was a positive development. We are now seeing the results of those efforts and there have been some nice discoveries. When evaluating an investment target we look for good infrastructure, accessible locations, and projects with prospective geology that promises to translate into robust ore deposits. Grade is generally king.

Looking at silver specifically, how do you see its industrial value as an influence in its supply and demand dynamic?

Silver is a fascinating metal because in addition to being one of the oldest forms of money, it has properties that make it highly useful in industrial applications. Silver is highly electricity conductive and ductile, so it’s widely used in electronics and is perfect for micro-electronic devices. Silver is one of Earth’s most reflective substances, so it is used in mirrors and makes beautiful jewellery and silverware.

Silver is well-known to have antibacterial properties and is used in medicine and consumer products to kill germs. Some of the most prospective and fast-growing applications are photovoltaics, automotive, and 5G connectivity. Solar accounts for about 10% of the market currently and is projected to continue growing as the world continues to seek clean energy alternatives and thrifting is reaching diminishing returns. In fact, more efficient solar panels use more silver, not less. Electric vehicles (EVs) are gaining traction worldwide leading to rapid growth in the auto sector because EVs have higher silver loadings than internal combustion engine cars. Finally, the transition to 5G networks and higher levels of telecommunication connectivity is leading to more silver demand.

So while there are headwinds for precious metals over the short term – not least high inflation – we remain sanguine that these safe-haven commodities will continue to attract investors and expect prices to rise as a consequence. I believe all of this bodes well for precious metals exploration in the future.

{kind=link}