Gold continues to deliver strong relative performance and is up 12.97% on a year-to-date basis through April 27, 2020, versus -10.36% for the S&P 500 Total Return Index.1

Through Close on Monday, April 27, 2020

| Asset | YTD | 1 YR | 3 YR* | 5 YR* |

| Gold Bullion | 12.97% | 33.10% | 10.65% | 7.33% |

| S&P 500 TR Index | -10.36% | -0.11% | 8.52% | 8.59% |

* Average annual total returns. Source: FactSet.

A Pile of Debt

Prior to Covid-19, the financial markets had become dependent on liquidity provided by central banks around the globe. The modest ~2% annual economic growth post the great financial crisis (“GFC”) was underpinned by constant monetary accommodation by the central banks, as well as by growing fiscal deficits. That combination served to extend the business cycle into one of the longest expansions on record, but at the cost of incalculable malinvestment and a record pile of debt which can never be repaid without more accommodation and financial repression.Gold is not only a financial hedge to government monetary and fiscal policies, but it is also a mandatory portfolio and household diversification asset.

“Gold is not only a financial hedge to government monetary and fiscal policies, but it is also a mandatory portfolio and household diversification asset.”

Like over-served party guests, not many investors or voters seemed concerned about the long-term implications of the build-up in debt to record levels against underlying GDP (gross domestic product), the unprecedented debt issuance by most sovereigns or the ballooning budget deficits. The strong suit of democracy has rarely been to encourage elected representatives to make good forward-looking decisions when they involve making present-day sacrifices.

Figure 1. The Cost of Financing the Credit Bubble

Source: Meridian Macro Research LLC. Data as of 3/31/2020.

COVID-19 Pandemic Pulls the Trigger

At the dawn of this new decade, the steady provision of liquidity had priced almost all markets to perfection:

- The S&P 500 was trading at a large premium to long-term valuation multiple ranges;

- There was a record portion of assets in funds managed primarily by computers;

- There was more debt trading at negative yields than at any time in history;

- There had been a 30-year bull market in bonds;

- Investment real estate was traded on the most levered basis and at the lowest cap rates;

- There was record debt at all levels on actual and percentage basis (government, corporate and personal);

- There was a record total of unfunded future liabilities;

- There had been unprecedented, coordinated intervention and accommodation in almost all financial markets by governments around the world over the past 1, 3, 5 and 10 years.

This bubble was popped when lockdowns were required to protect the population, and the vastly under-funded and unprepared healthcare systems, from the COVID-19 pandemic. Neither consumers, businesses, nor governments had the wherewithal to withstand an extended furlough, and the economic shockwaves quickly required emergency actions. The markets did not have enough liquidity to meet the sudden increase in volatility and corresponding de-leveraging, or the need for U.S. dollars for repayment and margin.

The New Era of Big Government

We are now entering a period in which public officials will control many more levers than in the past. Governments globally have pledged unlimited financial support for markets. We know that healthcare spending needs to ramp up significantly. Most governments have committed to supporting the pay of furloughed workers. We await government policies on emerging from this lockdown, which likely involve complicated start-up protocols and, inevitably, the promise of more fiscal stimulus

Super Bank to the Rescue

In the same spirit and once again, central planners have rushed to the rescue of the broader markets, consumers and specific industries. This time around, many economic sectors including retail, real estate, hospitality, travel, energy and high-yield banking all face major challenges. There is no appetite for austerity or consequences, only a tendency to fix every problem with a government-engineered solution.

Accordingly, many programs with new acronyms are forthcoming, a summary of which would be too lengthy to cite. The scale of this money printing, which by some counts will hit $7 trillion in the U.S. alone, is shocking in size and scope. It is difficult to follow how adding more short-term, Fed-guaranteed debt or securities purchases fixes a revenue problem for most businesses, workers and consumers affected by the shutdowns. We concede that one of the biggest problems in printing that much money is how to get it into the right hands.

We are clear on one thing: the Federal Reserve has been thrust into a new mandate with broadened scale and scope. Specifically, using its emergency authority under Section 13 (3) of the Federal Reserve Act, the Fed will now (a) indirectly lend to municipalities, companies and consumers, and (b) indirectly purchase securities of specific companies and (b) cooperate with the U.S. Treasury to provide virtually unlimited funding to the Treasury, bank, corporate and consumer markets. Two weeks ago, the Fed struck a new note by announcing that its 19 appointed officials will now pick securities for purchase, including “fallen angel” high-yield bonds.

Based on overwhelming odds that recovery will take some time, we have little doubt that the trillions of dollars already approved for stimulus will require hefty increases in the coming months.

Yield Curve Control

We at Sprott have previously remarked (see A Message from the CEO: This Tide Will Turn) that growing debt balances and skyrocketing budget deficits offered no possibility for interest rate normalization. We observed based on statistics from the U.S. Treasury auctions in the waning days of 2020 that the Fed was required to lap up unsold Treasury bond positions from the last series of auctions by exchanging dealer inventories for Fed liquidity as little as three days after the auctions settled.

What is now of greater interest is to understand how the U.S. Treasury intends to finance all of the newly announced programs on top of what was already a massive funding requirement. The proportion of Treasury issuance sterilized by the buying of foreign banks requiring f/x (foreign exchange) reserves has shrunk to immaterial, and likewise commercial banks were so full of Treasuries that repo support has been required to assist them since Q3 2019.

Fortunately, the Fed has confirmed that they will buy whatever it takes to swallow the supply of U.S. Treasuries at acceptable yields. This will require the Fed balance sheet to balloon to at least $11 trillion based on announced programs, while economists forecast numbers as high as $15-20 trillion in the event that the COVID-19 recovery takes longer to play out. Central banks in Europe, the UK, Japan, other G7 nations and China are on much the same trajectory.

Figure 2. The U.S. Fed Balance Sheet Climbs to $11 Trillion

Source: BCA Research. *Source: Bloomberg Barclays Indices. **Source: The U.S. Federal Reserve.

Certificates of Confiscation

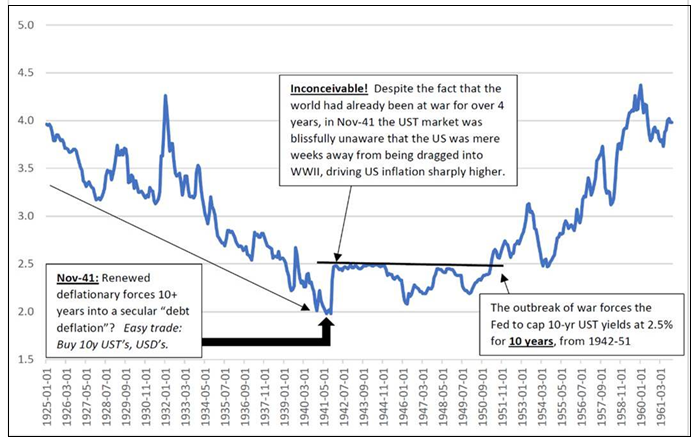

This tsunami of printing will crowd the market to such a level that it amounts to what could be seen as a quasi-nationalization of the sovereign bond markets. As Luke Gromen notes below, it would not be the first time that the government controlled the duration of the yield curve through debt monetization. Figure 3. shows the period during WWII throughout which the U.S. government effectively pinned its long rates, although at that time it was at a more reasonable 2%.

Figure 3. U.S. Long-Term Government Bond Yields (1925 – 1961)

Source: Luke Gromen. FFTT-LLC.

Consider though, that in addition to the creation of U.S. dollars required to fund their Treasury purchases, the Fed has added multiple swap programs to fulfill U.S. dollar seekers. Adding in the continued negative contribution from the U.S. balance of payments deficit, the world will soon be awash in U.S. dollars. As contrarians, we believe today’s U.S. inflation break-even rates under-estimate the potential for goods and labor price increases by late 2020, and that the U.S. dollar strength has largely run its course.

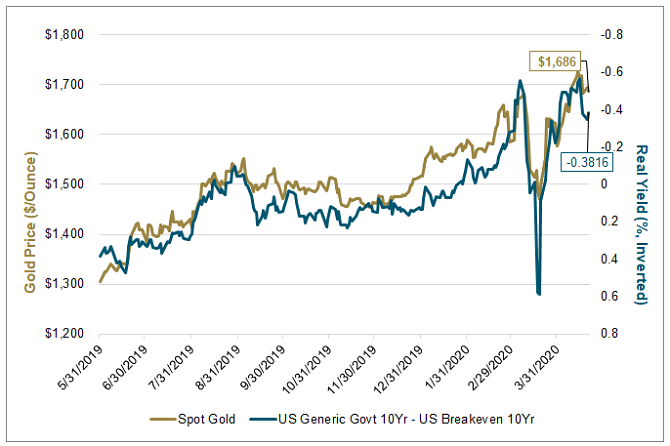

Figure 4. Negative Real Yields are Made of Gold

A resumed fall in inflation-adjusted yields pushed gold to a recent high.

Source: Bloomberg. Data as of 4/27/2020.

In summary, we propose that sovereign bonds will no longer function to provide real investment returns or as an effective equity hedge. Instead, they are likely to become a negative real return anchor to investors, with no upside and significant downside in the event of an inflationary environment. This has major implications for the gold market, in that we are likely to be relegated to an environment of negative real rates for the foreseeable future.

Gold in the New Era

We propose that gold is not only a financial hedge to government monetary and fiscal policies, it is a mandatory portfolio and household diversification asset. Gold provides a degree of separation from the ongoing debasement of all fiat currencies. While gold is a reportable and taxable asset in all developed countries, it is not subject to manipulated fiat currency and sovereign bond markets. We believe gold is, first and foremost, a store of value. We believe there is fundamental support for a qualified currency to exist outside of government-led debasement. Gold is multiples more legitimate and efficient than any other alternative currency.

Those comparing gold to a risk asset, as Warren Buffett and others have done, miss its true value. An allocation to gold starts as an allocation to an alternate form of cash. That allocation doesn’t become risk-bearing until you accept that your currency of choice needs be to be fiat. See Figure 5. below for the track record of the purchasing power of gold against the U.S. and other currencies.

Figure 5. Purchasing Power of Main Currencies Valued in Gold (1/1971-4/2020)

Major fiat currencies have lost significant value compared to gold (U.S. Dollar, Swiss Franc, British Sterling, Euro).

Source: Incrementum. Data as of 3/31/2020.

Gold Market Update

Our thesis for gold as an asset providing an insurance policy during a process of financial repression remains intact and has been accelerated by the current crisis. We cite two recent examples which provide evidence of gold’s tendency to increase its value when tested. First, we observed how the liquidity crisis and “USD margin call” of mid-March challenged all levered investors and gold held its value well while other markets crumbled.

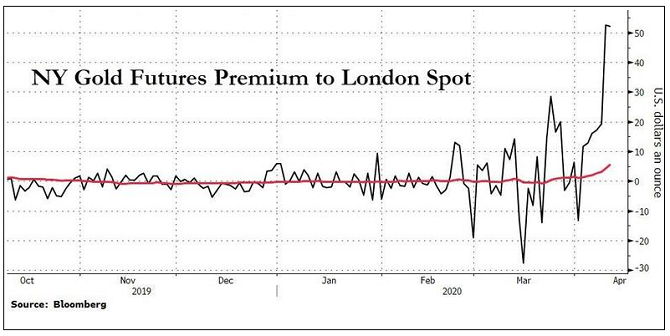

Second, recent changes in the physical gold bullion market have convinced us that buyers are increasingly demanding allocated physical storage and ability to deliver versus “paper gold” contracts. Recent interruptions in the physical gold markets are the function of short-term influences such as mine closures, refinery and mint shutdowns and challenging freight conditions. The volatility and quantum of premiums of the closest futures contract, and its backwardation to outside contracts, underscore a longer-term development in our view. Investors are clearly putting more scrutiny on their preference for physically-backed allocated storage versus cheaper and easier liquidity. At Sprott, we always advocate that investors only consider the former and markets are corroborating that view, with the result that the higher forward month may continue lead the spot and future prices higher.

Figure 6. Gap Between NY Futures and Spot Prices is Elevated

The internal mechanics of the gold market are again showing strains under this rally. The gap between New York futures and spot prices in London is still elevated, a sign of lingering concern over future supply of the physical form of the metal. (Source: Zerohedge.com)

Most technical charts show how well gold consolidated around the lower end of its uptrend channel in the midst of last month’s liquidity crisis, and continue to provide us with confidence that the trends are intact for $2,000 plus by late 2020/early 2021. We add that gold liquidity continues to be significant, for instance LBMA’s Q1 turnover increased about 25% to over $4 trillion.

Our Advice

Our advice remains the same, to overweight gold within your portfolio, and now do so within your household discretionary cash. One lasting effect of the crisis will be to remind us that we are human, and we require some protection from a world which had come to expect perfection. There is a need for insurance from the growing credit issues which will continue long after the health crisis.

To us, that means most investors should be 5-10% exposed to precious metals. For those willing to seeking to play offense, consider the purchase of quality and emerging gold equities. They have not yet moved significantly and provide leverage gold reserves, and to businesses which are entering into a period of record operating margins.

We are grateful that Sprott as a firm is functioning better than ever before. We have a strong financial position, and technologically able to handle our investment portfolios and account inquiries remotely on a global basis, and are operating safely in this virtual environment. We remain available to answer your questions and to earn your business. Please reach out to Client Services at 888.622.1813.

Sincerely,

Peter Grosskopf

Chief Executive Officer,

Sprott Inc.

Client Services Contact Information

Telephone: 888.622.1813

Email: invest@sprott.com

Investor Contact Information

Glen Williams

Managing Director, Investor Relations & Corporate Communications

Telephone: 416.943.4394

Email: gwilliams@sprott.com

Media Contact Information

Dan Gagnier/Jeff Mathews

Gagnier Communications

Telephone: 646.569.5897

Email: sprott@gagnierfc.com

{kind=link}